JKH records strong recurring EBITDA of Rs.15.91

billion in Q4 2024/25

Summarised below are the key operational and financial highlights during the year under review.

- The year under review has been a pivotal one for the Group, marked by bold investments coming to fruition with the successful launch of two of the Group’s most ambitious and largest investments to date – City of Dreams Sri Lanka and the West Container Terminal (WCT-1) at the Port of Colombo. These landmark developments represent transformative opportunities, poised to serve as catalysts for economic growth, reinforcing Sri Lanka’s position as a logistics and leisure hub in the region.

- The Group’s financial performance remained in line with our expectations, driven by the strength of our consumer-focused businesses which gained momentum quarter after quarter. As anticipated, overall Group EBITDA was affected by the substantial pre-opening, ramp-up, and operating expenses at the City of Dreams Sri Lanka integrated resort.

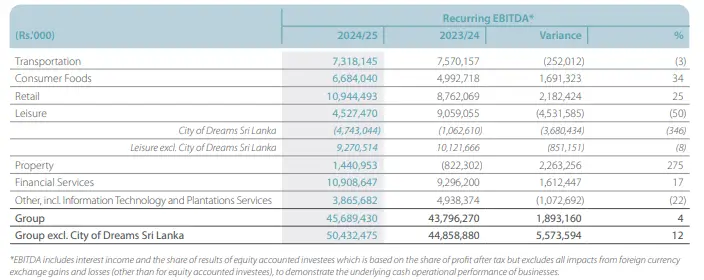

- Recurring EBITDA, excluding City of Dreams Sri Lanka, is an increase of 12% to Rs.50.43 billion against the comparative period [2023/24: Rs.44.86 billion], demonstrating the steady growth in the underlying businesses.

- Group recurring PBT, excluding City of Dreams Sri Lanka, stood at Rs.22.93 billion, a 60% increase against the comparative period [2023/24: Rs.14.36 billion].

-

The Cinnamon Life hotel is currently fully operational with the launch of all

restaurants and bars, conferencing spaces and outdoor locations. The hotel has been

positively received by the market, both locally and internationally, with

encouraging demand and bookings for the various spaces at the property. The

completion of the remaining elements of

the City of Dreams Sri Lanka integrated resort project is progressing well, with the fit-out and finishing works relating to the 113-key Nuwa hotel and the casino near complete for its planned opening in August 2025. - WCT-1, the Port of Colombo’s first automated deep-water terminal, and a milestone project for the Group, commenced its first phase of commercial operations in 4Q 2024/25. The throughput to date has been encouraging and this momentum is expected to accelerate over the coming quarters.

- Despite the translation impact of a stronger Rupee compared to the previous financial year, the profitability of SAGT recorded an increase driven by a 14% growth in volumes and an improvement in the mix. LMS recorded a strong volume growth of 15%, although profitability was impacted due to a contraction in margins mainly on account of intensified competition and a temporary oversupply of inventory.

- The significant increase in the Consumer Foods EBITDA is attributable to both the Beverages and Confectionery businesses, driven by volume growth and improved margins.

- The Supermarket business recorded a strong performance during the year, with same store sales recording a growth of 14.2% on the back of increased customer footfall.

- John Keells CG Auto (JKCG) established its New Energy Vehicles (NEV) business during the year, and the pipeline of vehicle bookings received by JKCG for its BYD NEV range is significantly higher than expected. Based on the current order book and expectations of deliveries in the ensuing quarter, the earnings are expected to be material in the context of the Group’s performance.

- The Sri Lankan Resorts segment recorded an increase in profitability on the back of a sustained recovery in tourist arrivals to the country, although offset by a decrease in profitability in the Maldivian Resorts and Colombo Hotels segments, mainly due to one-off impacts.

- The Property industry group recorded an increase in profitability driven by sales at Cinnamon Life and VIMAN development projects, and profit recognition from real estate sales in Digana, through Rajawella Holdings (Private) Limited.

- NTB recorded a strong growth in profitability on account of robust loan growth,

while UA recorded a growth of 15% in its gross written

premiums, stemming from an increase in renewal premiums and regular new business premiums. - The Group’s carbon footprint per million rupees of revenue, inclusive of the expanded operational boundary, increased by 7%. In contrast, water withdrawal per million rupees of revenue decreased by 8%.

- Following the success of deployed use cases, particularly in Supermarket, Confectionery, and Beverages, a roadmap for advanced analytics use cases was developed for the Transportation, Leisure and Insurance businesses during the year. Encouraging progress from these use cases affirms that the material value observed during pilot studies can be maintained at scale.

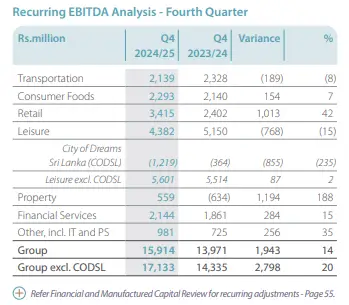

- The Group reported a strong performance for Q4, driven by the strength of our consumer-focused businesses which gained momentum quarter after quarter. Overall Group EBITDA was mainly impacted by the substantial pre-opening, ramp-up, and operating expenses at the CODSL.

- WCT-1, the Port of Colombo’s first automated deep-water terminal, and a milestone project for the Group, commenced its first phase of commercial operations in Q4 2024/25. The throughput to date has been encouraging and this momentum is expected to accelerate over the coming quarters.

- Group PBT, excluding CODSL, is Rs.10.85 billion, a 71% increase against Q4 2023/24. CODSL includes the depreciation charge and interest expense in the income statement pertaining to the Cinnamon Life hotel, amounting to Rs.1.14 billion and Rs.1.09 billion.

- The Transportation industry group recorded a decline in EBITDA mainly due to the

Bunkering business, Lanka Marine Services (LMS).

LMS recorded an improvement in margins, although the decline in volumes by 17% impacted earnings growth. It is noted that Q4 of 2023/24 was an exceptionally strong quarter on account of a

significant growth in volumes over 50% due to the Red Sea crisis. The Group’s Ports and Shipping business, South Asia Gateway Terminal (SAGT) recorded volume growth and an improvement in volume mix although profitability was flat due to the appreciation of the Rupee. - The Consumer Foods industry group recorded a strong growth in profitability driven by double-digit volume growth across all businesses, driven by seasonal sales and a continued recovery in consumer activity. Margins of the Beverages and Confectionery businesses marginally declined due to the increase in excise duties on carbonated soft drinks, effective from 1 January 2025 for the Beverages business, a relatively lower growth in Impulse volumes which comprise of higher margin products and an increase in advertising and promotion expenses in the Confectionery business.

- The significant increase in profitability in the Supermarket business is attributable to the strong same store sales growth of 16.2% on the back of an increase in footfall of 19.1%, which more than offset the negative average basket value (ABV) growth of 2.4%.

- The profitability of the Leisure industry group was impacted by substantial costs pertaining to the opening and operating of the Cinnamon Life hotel. Excluding the City of Dreams of Sri Lanka, Leisure EBITDA was flat at Rs.5.60 billion.

- Excluding the impact of CODSL, the profitability of the Leisure industry group was

driven by a strong recovery in arrivals which resulted in higher occupancy and an

improvement in average room rates (ARRs) across the Group’s hotel portfolio. Margins

of the businesses were mainly supported by the improvement in rates and

occupancies,

and lower operating costs, despite the translation impact due to the appreciation of the Rupee. - The Property industry group recorded an increase in profitability driven by sales at Cinnamon Life and the VIMAN development project, and profit recognition from real estate sales in Digana, through Rajawella Holdings (Private) Limited. It should be noted that EBITDA in Q4 2023/24 included an asset write-off amounting to Rs.639 million relating to the closure and demolishing of the K-Zone mall in Ja-Ela for the development of the VIMAN residential project.

- Nations Trust Bank PLC recorded a growth in profitability driven by robust loan growth. Union Assurance PLC recorded encouraging double-digit growth in gross written premiums, driven by renewal premiums and regular new business premiums.

- The Other, including Information Technology and Plantation Services sector recorded an increase in EBITDA mainly due to exchange gains recorded at the Holding company compared to exchange losses in Q4 2023/24 due to the appreciation of the Rupee. Despite the increase in borrowings at the Holding Company, PBT recorded an improvement on account of a decrease in finance expenses at the Holding Company as a result of the lower interest cost on the convertible debentures issued to HWIC Asia Fund compared to Q4 2023/24, as the debentures were fully converted in January 2025.

JKH records strong recurring EBITDA of Rs.15.91

billion in Q4 2024/25

Summarised below are the key operational and financial highlights during the year under review.

- The year under review has been a pivotal one for the Group, marked by bold investments coming to fruition with the successful launch of two of the Group’s most ambitious and largest investments to date – City of Dreams Sri Lanka and the West Container Terminal (WCT-1) at the Port of Colombo. These landmark developments represent transformative opportunities, poised to serve as catalysts for economic growth, reinforcing Sri Lanka’s position as a logistics and leisure hub in the region.

- The Group’s financial performance remained in line with our expectations, driven by the strength of our consumer-focused businesses which gained momentum quarter after quarter. As anticipated, overall Group EBITDA was affected by the substantial pre-opening, ramp-up, and operating expenses at the City of Dreams Sri Lanka integrated resort.

- Recurring EBITDA, excluding City of Dreams Sri Lanka, is an increase of 12% to Rs.50.43 billion against the comparative period [2023/24: Rs.44.86 billion], demonstrating the steady growth in the underlying businesses.

- Group recurring PBT, excluding City of Dreams Sri Lanka, stood at Rs.22.93 billion, a 60% increase against the comparative period [2023/24: Rs.14.36 billion].

-

The Cinnamon Life hotel is currently fully operational with the launch of all

restaurants and bars, conferencing spaces and outdoor locations. The hotel has been

positively received by the market, both locally and internationally, with

encouraging demand and bookings for the various spaces at the property. The

completion of the remaining elements of

the City of Dreams Sri Lanka integrated resort project is progressing well, with the fit-out and finishing works relating to the 113-key Nuwa hotel and the casino near complete for its planned opening in August 2025. - WCT-1, the Port of Colombo’s first automated deep-water terminal, and a milestone project for the Group, commenced its first phase of commercial operations in 4Q 2024/25. The throughput to date has been encouraging and this momentum is expected to accelerate over the coming quarters.

- Despite the translation impact of a stronger Rupee compared to the previous financial year, the profitability of SAGT recorded an increase driven by a 14% growth in volumes and an improvement in the mix. LMS recorded a strong volume growth of 15%, although profitability was impacted due to a contraction in margins mainly on account of intensified competition and a temporary oversupply of inventory.

- The significant increase in the Consumer Foods EBITDA is attributable to both the Beverages and Confectionery businesses, driven by volume growth and improved margins.

- The Supermarket business recorded a strong performance during the year, with same store sales recording a growth of 14.2% on the back of increased customer footfall.

- John Keells CG Auto (JKCG) established its New Energy Vehicles (NEV) business during the year, and the pipeline of vehicle bookings received by JKCG for its BYD NEV range is significantly higher than expected. Based on the current order book and expectations of deliveries in the ensuing quarter, the earnings are expected to be material in the context of the Group’s performance.

- The Sri Lankan Resorts segment recorded an increase in profitability on the back of a sustained recovery in tourist arrivals to the country, although offset by a decrease in profitability in the Maldivian Resorts and Colombo Hotels segments, mainly due to one-off impacts.

- The Property industry group recorded an increase in profitability driven by sales at Cinnamon Life and VIMAN development projects, and profit recognition from real estate sales in Digana, through Rajawella Holdings (Private) Limited.

- NTB recorded a strong growth in profitability on account of robust loan growth,

while UA recorded a growth of 15% in its gross written

premiums, stemming from an increase in renewal premiums and regular new business premiums. - The Group’s carbon footprint per million rupees of revenue, inclusive of the expanded operational boundary, increased by 7%. In contrast, water withdrawal per million rupees of revenue decreased by 8%.

- Following the success of deployed use cases, particularly in Supermarket, Confectionery, and Beverages, a roadmap for advanced analytics use cases was developed for the Transportation, Leisure and Insurance businesses during the year. Encouraging progress from these use cases affirms that the material value observed during pilot studies can be maintained at scale.

- The Group reported a strong performance for Q4, driven by the strength of our consumer-focused businesses which gained momentum quarter after quarter. Overall Group EBITDA was mainly impacted by the substantial pre-opening, ramp-up, and operating expenses at the CODSL.

- WCT-1, the Port of Colombo’s first automated deep-water terminal, and a milestone project for the Group, commenced its first phase of commercial operations in Q4 2024/25. The throughput to date has been encouraging and this momentum is expected to accelerate over the coming quarters.

- Group PBT, excluding CODSL, is Rs.10.85 billion, a 71% increase against Q4 2023/24. CODSL includes the depreciation charge and interest expense in the income statement pertaining to the Cinnamon Life hotel, amounting to Rs.1.14 billion and Rs.1.09 billion.

- The Transportation industry group recorded a decline in EBITDA mainly due to the

Bunkering business, Lanka Marine Services (LMS).

LMS recorded an improvement in margins, although the decline in volumes by 17% impacted earnings growth. It is noted that Q4 of 2023/24 was an exceptionally strong quarter on account of a

significant growth in volumes over 50% due to the Red Sea crisis. The Group’s Ports and Shipping business, South Asia Gateway Terminal (SAGT) recorded volume growth and an improvement in volume mix although profitability was flat due to the appreciation of the Rupee. - The Consumer Foods industry group recorded a strong growth in profitability driven by double-digit volume growth across all businesses, driven by seasonal sales and a continued recovery in consumer activity. Margins of the Beverages and Confectionery businesses marginally declined due to the increase in excise duties on carbonated soft drinks, effective from 1 January 2025 for the Beverages business, a relatively lower growth in Impulse volumes which comprise of higher margin products and an increase in advertising and promotion expenses in the Confectionery business.

- The significant increase in profitability in the Supermarket business is attributable to the strong same store sales growth of 16.2% on the back of an increase in footfall of 19.1%, which more than offset the negative average basket value (ABV) growth of 2.4%.

- The profitability of the Leisure industry group was impacted by substantial costs pertaining to the opening and operating of the Cinnamon Life hotel. Excluding the City of Dreams of Sri Lanka, Leisure EBITDA was flat at Rs.5.60 billion.

- Excluding the impact of CODSL, the profitability of the Leisure industry group was

driven by a strong recovery in arrivals which resulted in higher occupancy and an

improvement in average room rates (ARRs) across the Group’s hotel portfolio. Margins

of the businesses were mainly supported by the improvement in rates and

occupancies,

and lower operating costs, despite the translation impact due to the appreciation of the Rupee. - The Property industry group recorded an increase in profitability driven by sales at Cinnamon Life and the VIMAN development project, and profit recognition from real estate sales in Digana, through Rajawella Holdings (Private) Limited. It should be noted that EBITDA in Q4 2023/24 included an asset write-off amounting to Rs.639 million relating to the closure and demolishing of the K-Zone mall in Ja-Ela for the development of the VIMAN residential project.

- Nations Trust Bank PLC recorded a growth in profitability driven by robust loan growth. Union Assurance PLC recorded encouraging double-digit growth in gross written premiums, driven by renewal premiums and regular new business premiums.

- The Other, including Information Technology and Plantation Services sector recorded an increase in EBITDA mainly due to exchange gains recorded at the Holding company compared to exchange losses in Q4 2023/24 due to the appreciation of the Rupee. Despite the increase in borrowings at the Holding Company, PBT recorded an improvement on account of a decrease in finance expenses at the Holding Company as a result of the lower interest cost on the convertible debentures issued to HWIC Asia Fund compared to Q4 2023/24, as the debentures were fully converted in January 2025.

Latest News

John Keells Foundation marks its 21st anniversary with a redesigned website and new Volunteer App

31 March, 2026

John Keells Holdings PLC Recognised Across Sectors at the ACCA Sustainability Reporting Awards 2024/25

25 March, 2026

John Keells Holdings PLC Recognised for Showcasing Excellence in Corporate Reporting at the TAGS Awards 2025

25 February, 2026

John Keells Holdings PLC was recognised as one of the Top 10 Best Employers at the EFC National Best Employer Awards 2025

05 February, 2026